Import Data - September 2023

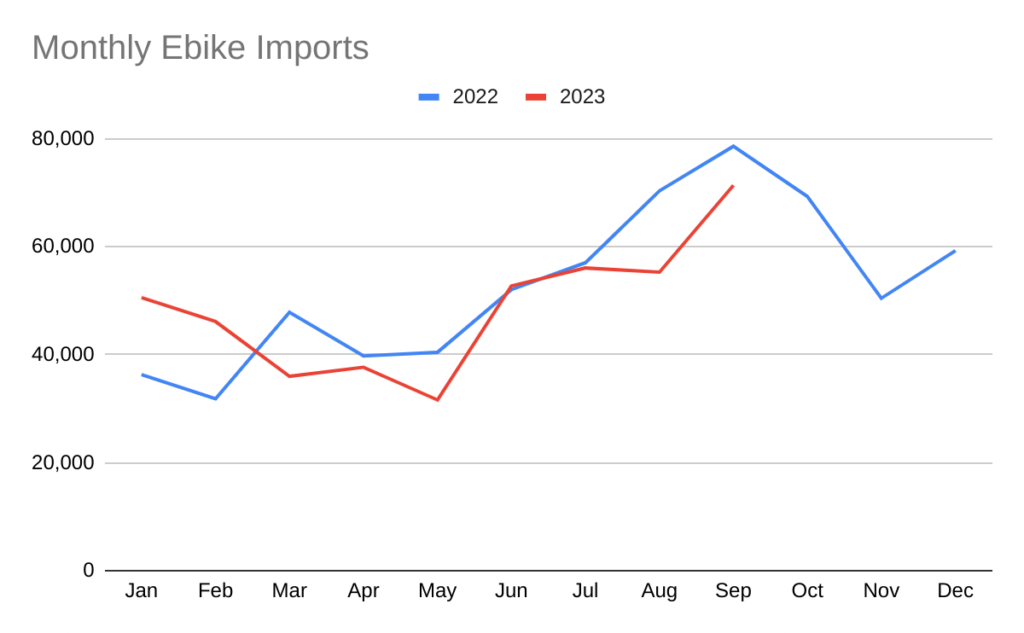

Autumnal increases in ebikes

The chart above shows monthly imports of ebikes comparing the last two years. We can se there is a seasonal increase in units, which declines as we move into Q4. This is likely to be in anticipation of holiday sales, as it may take a bit of time for the products to work their way through the supply chain within the united states.

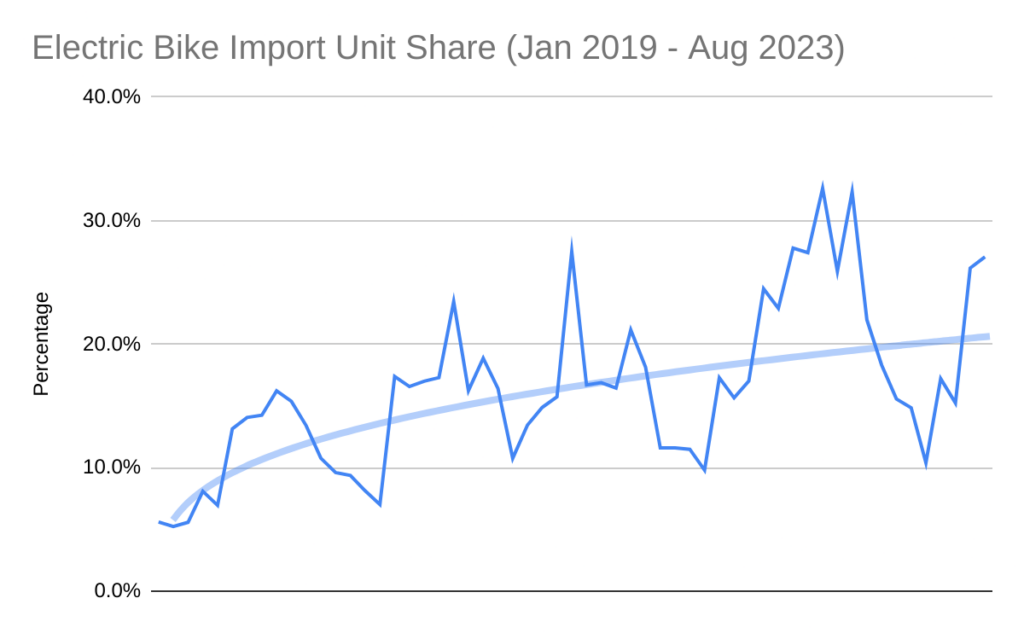

A note on specific import quantities

When comparing our dataset to data from the USITC tarrif data, there are notable differences. 2023 H1 data matches well at ~1.4m units, but 2022 H1 data is divergent quite a bit. As reported in Bicycle Retailer and Industry News, average bike prices jumped 60% in H1 2023, indicating that the bikes imported last year were of lower value (~$140/bike). Many of these bikes are likely to be smaller children's bikes, which are easier to group together into bulk packages. Although we can expect that most brands will report accurate bike quantities to government authorities, they may only report bulk grouping quantities on shipping manifests.

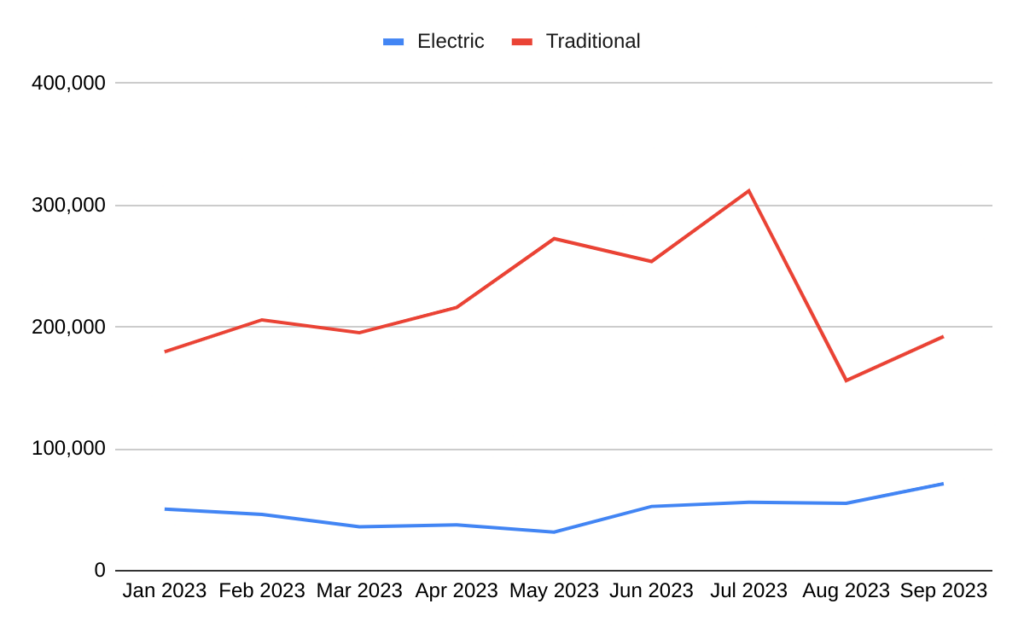

Rebounding Traditional Bikes

Last month we reported on a precipitous drop in traditional bike imports due to a major importer pulling back. This number has rebounded slightly to similar levels seen in January. However, this drop combined with the gains seen in electric bikes have pushed the monthly ratio to 27% electric bikes. Traditional bike imports YTD appear to be up slightly at 1.3% in our data set

| Month | Electric | Traditional | Electric Import Share |

| Jan 2023 | 50,560 | 179,678 | 22.0% |

| Feb 2023 | 46,132 | 205,907 | 18.3% |

| Mar 2023 | 35,999 | 195,368 | 15.6% |

| Apr 2023 | 37,656 | 216,028 | 14.8% |

| May 2023 | 31,613 | 272,576 | 10.4% |

| Jun 2023 | 52,733 | 253,823 | 17.2% |

| Jul 2023 | 56,053 | 311,869 | 15.2% |

| Aug 2023 | 55,290 | 156,106 | 26.2% |

| Sep 2023 | 71,348 | 192,333 | 27.1% |