This blog post will analyze 14 months of data on peer-to-peer marketplaces showing second hand bicycles for sale from September 2023 through October 2024. The data has been collected directly from marketplaces, and represents a fairly unique view of used bicycle markets. The primary other research into this area is our project with People For Bikes in the United States, which will be expanding to trade-in platforms this month. To see data about the USA, reach out to People For Bikes, or send me an email.

High level market view

Overall, we observed ~150,000 bicycle units sold on peer to peer marketplaces over the past year. These marketplaces include eBay, Facebook, and Gumtree. As can be seen above, this fall is experiencing greater sales than 2023. Keep in mind that the Australian cycling seasonal curve is roughly the opposite of the North America and Europe, with peak season in December.

Interestingly, new inventory listings do not follow the same curve as sales. In the same 12 month period, ~312,000 units were listed for sale, suggesting a 48% sell through rate. Some people will wonder what happens to those other bikes. It is important to keep in mind that these are peer-to-peer marketplaces where nearly all sellers are individuals not acting as a business. This is crucial because and individual holds a certain utility value in the bike. That is to say, they could ride the bike, save it for a friend, or otherwise use it. Additionally, since this is not their primary source of income, they are less likely to overcome transactional friction. If it is too difficult to sell, or the price is too low, they may simply keep it in their garage.

The above chart shows how new listings do not follow the same seasonal trend as sales. In fact, there has been a slight downward trajectory for inventory listing units. One of the big reasons for the discrepancy is the different incentive reactions between buyers and sellers. As the following chart shows, prices have fallen more than 25% over the past year. Simple economics would predict that more buyers would be attracted, while sellers would be dissuaded. And that is exactly what we are seeing in the Australian Market.

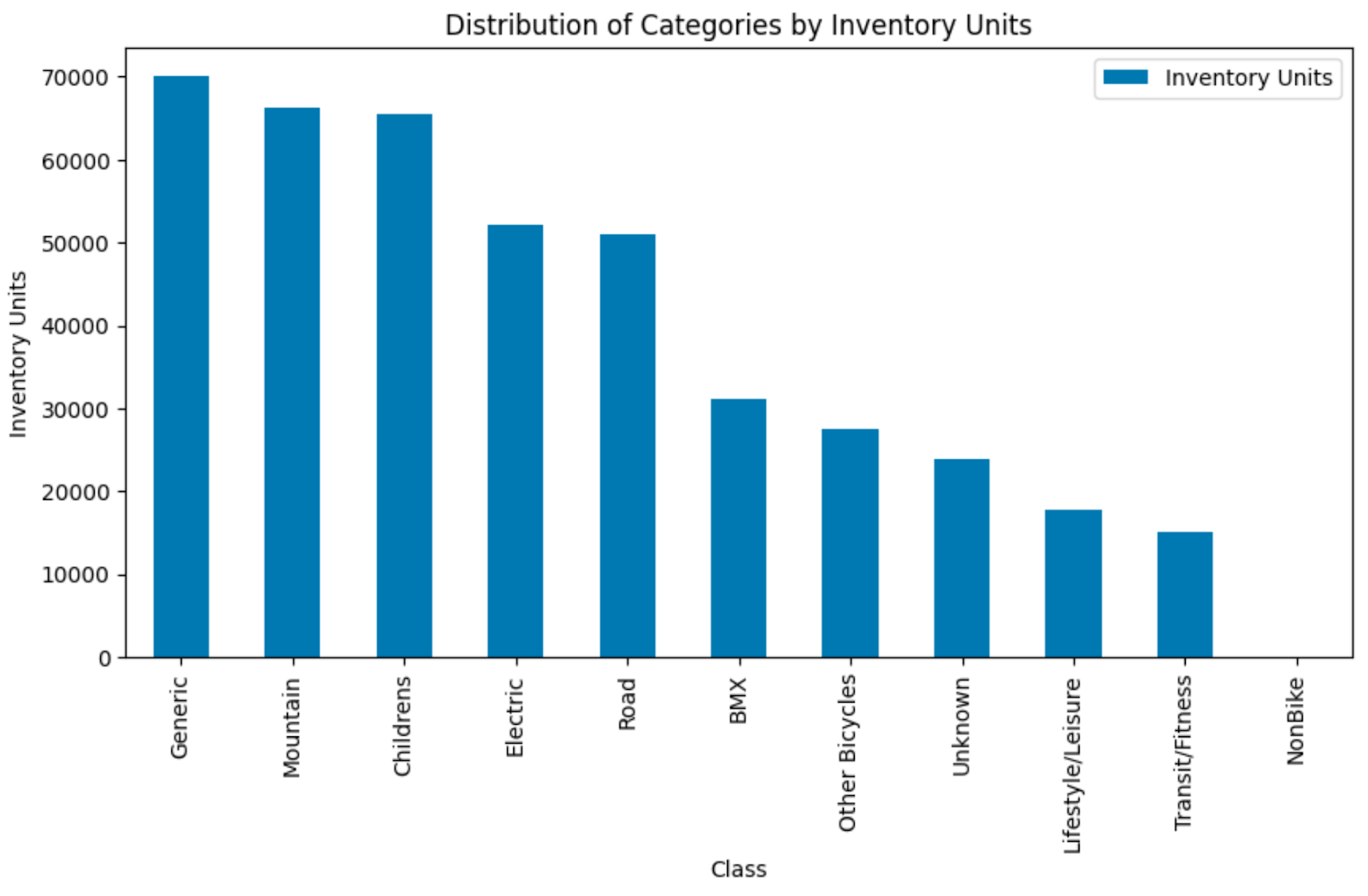

Categories and Marketplaces

Above we see how dominant Facebook Marketplace is in the Australian market. Neither Ebay, nor Gumtree are able to compete to any substantial rate. This is due to the lower transactional friction in listing on Facebook. According to NapoleonCat Statistics, nearly 83% of Australians have a Facebook account. This makes it very easy to list on the platform by skipping the sign up step. Secondly, the platform does not currently charge a transaction fee. In many ways, this is a help. However, eBay has carved out a niche by offering more premium road and Mountain bikes where the transaction fee acts as a filter for legitimate buyers and sellers.

Next, if we look at the distribution of inventory units by category, we can see that the largest group are bikes listed in a generic fashion. These are listings where the title does not give away the type of bike, such as “Adult Bike” or “Bike for Sale”.

The major emerging category in the world of bicycles are electric bikes. Since data of retail sales in Australia is majorly lacking, we can look at the share of bicycle units in peer to peer marketplaces as an indicator of the sales over the past few years. The pie chart below shows that Australia is lagging behind most European countries at only 12.4% of units. Some research I have done on US imports indicates that in the US close to 20% of adult bikes are electric.

If we adjust our figures and ignore children’s, BMX, unknown, and generic categories, the figures look decidedly different. Looking below, listings exceed 22% and sales are just over 29% of total units. Most likely this is an over estimate of the actual consumer share of bicycles. Nonetheless it serves as an informative look at how many Australian cyclists are riding electric bikes.

Below left we can see the overall distribution of prices for electric bikes on these platforms. Clearly low price points are favored. However, this histogram is not that useful at this wide view, so below right we can see the breakdown of prices below $1,000. Here we can see a much more linear relationship between price and listing volumes. There are some notable bumps below $100, around $500, and around $750. These specific price points are likely to be anchored by consumers on common round price points thought to be preferred.

Below we can see that while listing prices have fallen throughout the year, just like the broader market, selling prices have fluctuated seasonally at a stable trend. The bottom right chart helps to explain this where we can see the gap between listing and selling average prices has contracted. The 50% variance at the beginning of the period was exceptionally high, indicating that consumers of second hand bikes are more interested in lower prices, while sellers expected higher prices. The ending 35% variance is more in line with other markets observed.

How large is the Australian second hand bicycle market?

This data shows that the Australian peer-to-peer online marketplaces generated around $12 million AUD over the past 12 months. Depending on the amount of sales of second hand bikes by retailers and in person swap meets, the total second hand market in Australia is likely under $30 million AUD. However, we do not have any data for retail sales, nor in person sales, so we would need to differ to experts in the Australian field to make those extrapolations. Nevertheless, the $12m peer to peer sales can serve as an anchor for further discussions to define the total market size and composition of the Australian bicycle market